The Affordable Care Act is providing women with an impressive array of reproductive health care options – except where it doesn’t.

Whether a woman is benefitting from the ACA depends very much on her address, and the rather complicated workings of state exchanges. But with some caveats, for Connecticut women, the law is working.

We should take a moment to think about that. Connecticut women are in the unusual position of having an important political promise met. As for much of the rest of the country, well…

At the request of the House Republican leadership, the Government Accountability Office issued a report in mid-September that examined how qualified health plans under the ACA provide coverage for abortion services around the country. The report underscores how abortion has been put into a separate class of medical care, with a maze of regulations and lack of clarity.

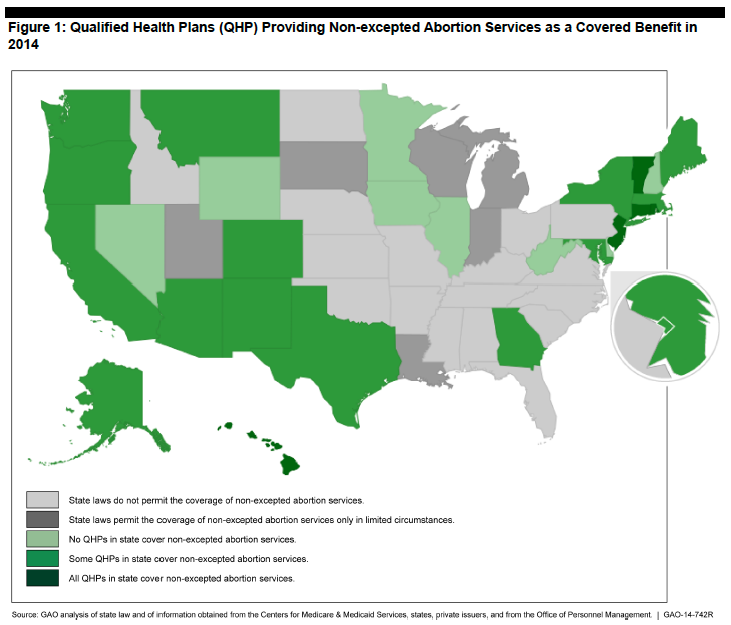

Results in the GAO report were mixed. At the time of the report, 23 states had laws that restrict insurance companies from offering abortion coverage except under certain circumstances, such as rape or incest. Add to those 23 Arizona and Georgia, both of which have passed abortion coverage restrictions.

GAO report

In Connecticut, all qualified health plans provide non-excepted abortion services.

Twenty-six states (including the District of Columbia) have no such restrictions. Of those 26, just five – Connecticut among them — cover abortions without restricting coverage to rape, incest, or the pregnant woman’s health. In 13 states, most health plans offer abortion coverage through their exchanges. Eight states, despite not having laws that ban or restrict abortion coverage, offer no plan that covers abortion services.

No state requires all plans to offer coverage.

The Affordable Care Act prohibits federal funds going for abortion services, except when the terminated pregnancy is a result of rape or incest, or when the pregnant woman’s life is in danger. Meanwhile, it’s perfectly legal for health plans to cover abortion services with no restrictions – insurance companies have done so for decades. And let’s not get started on the requirement that insurance companies that offer unrestricted abortion coverage must collect two separate premiums – one to cover abortion, and one for the rest of the plan’s health services.

Confused yet?

“This is a pretty complicated area,” said Susan Yolen, vice president of public policy and advocacy at Planned Parenthood of Southern New England. “It’s hard for people to understand what’s really required in the ACA in the first place, how all of that is to be implemented, and whose job is to implement it. There are a lot of moving parts, but it’s vital that women are able to access plans that cover abortion, since over 40 percent of American women seek an abortion during their reproductive lives.”

Some of the confusion springs from the bad-idea compromises hatched to get the law passed in the first place. Back in 2009, when the fate of Obamacare hung in the balance, President Barack Obama bowed to anti-abortion forces and signed an executive order that prohibited federal money from paying for abortions.

The irony is that insurance companies have long covered abortions. Even Medicaid covered the procedure until 1977, when the Hyde Amendment – named for Rep. Henry Hyde, a voracious anti-abortion activist – closed off most Medicaid funding for abortion services.

That amendment has been disastrous for low-income women. In 1980, when the Supreme Court ruled in favor of the amendment, Justice Thurgood Marshall wrote in a dissent that “the predictable result of the Hyde Amendment will be a significant increase in the number of poor women who will die or suffer significant health damage because of a inability to procure necessary medical services.”

To add to the confusion, insurance customers don’t always know if they’re covered for abortions when they shop for a plan. According to the report, the ACA has no rules for insurers to notify enrollees about abortion coverage. Several insurers told the GAO that they don’t make that information readily available.

Customers need to call the company directly. Imagine if you will, treating information about insurance coverage of any other medical procedure – a bypass, a knee replacement – with the same lack of clarity. That simply would not happen.